Georgia Residents Struggle to Afford High Healthcare Costs; COVID Fears Add to Support for a Range of Government Solutions Across Party Lines

Key Findings

A survey of more than 950 Georgia adults, conducted from April 12, 2021 to May 3, 2021, found that:

- Almost 7 in 10 (68%) experienced healthcare affordability burdens in the past year;

- 4 in 5 (80%) are worried about affording healthcare in the future;

- Over half (56%) are worried about affording treatment for COVID-19 if they need it; and

- Across party lines, respondents express strong support for government-led solutions.

Survey context: A month prior to the survey period (on March 25, 2021), all Georgians ages 16 and older were made eligible to receive the COVID-19 vaccine.1 The percent of Georgians who had received at least one vaccine dose grew from 31% to 35% during the survey period, while new COVID-19 cases, hospitalizations and deaths dropped steadily.2 However, some Georgia counties continued to see a high number of COVID deaths and hospitalizations relative to their population.3 Also during this time, Georgia’s Governor lifted many COVID-19 rules for businesses, eliminating requirements for social distancing and masked employees.4

A Range of Healthcare Affordability Burdens

Like many Americans, Georgia adults currently experience hardship due to high healthcare costs. All told, almost 7 in 10 (68% of) Georgia adults experienced one or more of the following healthcare affordability burdens in the prior 12 months:

1) Being Uninsured Due to High Premium Costs

Almost half (48%) of uninsured adults cited “too expensive” as the major reason for not having coverage, far exceeding other reasons like “don’t need it” and “don’t know how to get it.”

2) Delaying or Forgoing Healthcare Due to Cost

Over half (58%) of Georgia adults encountered one or more cost-related barriers to getting healthcare during the prior 12 months, including:

- 38%—Cut pills in half, skipped doses of medicine or did not fill a prescription5

- 38%—Skipped a recommended medical test or treatment

- 36%—Delayed going to the doctor or having a procedure done

- 34%—Skipped needed dental care

- 33%—Avoided going to the doctor or having a procedure done altogether

- 29%—Had problems getting mental healthcare or addiction treatment

Moreover, cost was by far the most frequently cited reason for not getting needed medical care, exceeding a host of other barriers like transportation, difficulty getting an appointment and lack of child care.

Of the various types of medical bills, the ones most frequently associated with an affordability barrier were dental bills, doctor bills and prescription drugs, likely reflecting the frequency with which Georgia adults seek these services—or, in the case of dental, perhaps lower rates of coverage for these services.

3) Struggling to Pay Medical Bills

Other times, Georgia adults got the care they needed but struggled to pay the resulting bill. Half (50%) of Georgia adults experienced one or more of these struggles to pay their medical bills:

- 19%—Contacted by a collection agency

- 17%—Unable to pay for basic necessities like food, heat or housing

- 16%—Used up all or most of their savings

- 16%—Borrowed money, got a loan or another mortgage on their home

- 12%—Racked up large amounts of credit card debt

- 10%—Placed on a long-term payment plan

High Levels of Worry About Affording Healthcare in the Future

Georgia adults also exhibit high levels of worry about affording healthcare in the future. Overall, 4 in 5 (80%) report being “worried” or “very worried” about affording some aspect of healthcare in the future, including:

- 63%—Cost of affording nursing home or home care services

- 63%—Health insurance will become too expensive

- 62%—Medical costs in the event of a serious illness or accident

- 61%—Medical costs when elderly

While two of the most common worries—affording the cost of nursing home or home care services and medical costs when elderly—are applicable solely to an older population, they were most frequently reported by respondents ages 35-44, followed by respondents ages 45-54. This finding indicates that residents may be worried about affording the cost of care for aging parents, in addition to themselves.

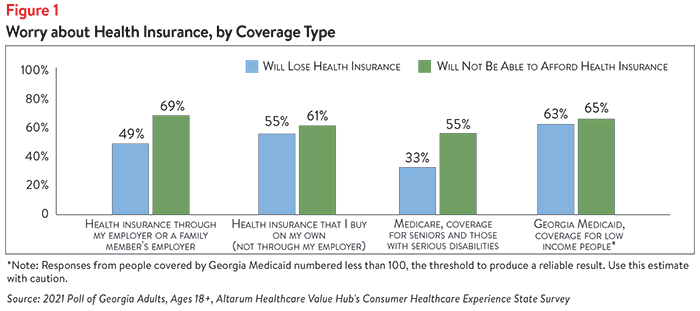

Furthermore, 47% of respondents of all ages are “worried” or “very worried” about losing their health insurance. These concerns vary by type of insurance coverage, with people who buy insurance on their own and those on Medicaid being most concerned about losing their coverage. Concerns about affording health insurance exceeded fears about losing coverage across all insurance types (see Figure 1).

Income Differences in Healthcare Affordability Burdens

The survey also revealed income differences in how Georgia adults experience healthcare affordability burdens.

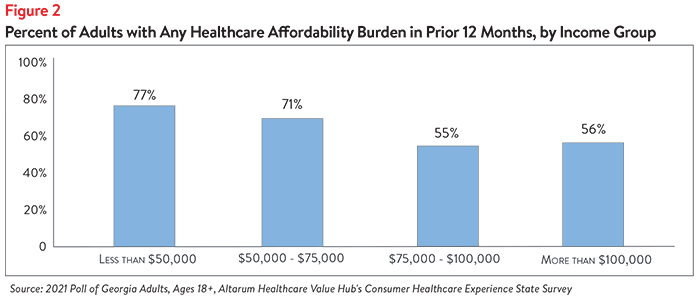

Affordability burdens affect families quite far up the income ladder, with over half (56%) of residents with household incomes of $100,000 or more struggling to afford healthcare in the past 12 months (see Figure 2). Georgia residents earning less than $50,0006 face the greatest burden, with 77% reporting affordability problems.

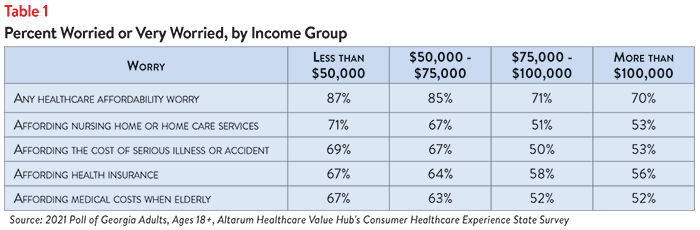

People with household incomes of less than $50,000 also report higher levels of worry about affording healthcare costs in the future; however, even residents earning more than $100,000 per year are worried about affording coverage and care (see Table 1).

COVID Worries

In addition to affordability worries, Georgia adults were asked about their top worries related to the COVID crisis.7 When asked about “affording treatment of coronavirus/COVID-19 if you need it,” 56% of respondents were somewhat worried or very worried.

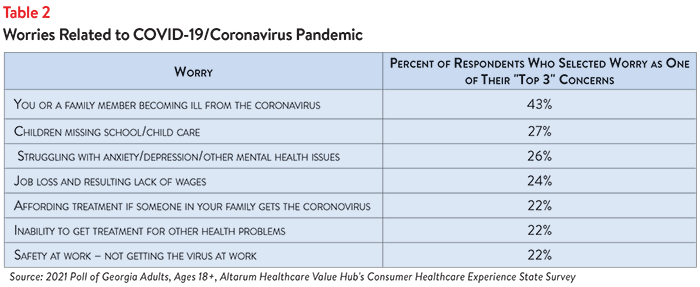

Separately, out of twelve possible responses, respondents were asked to pick the top three things they were most worried about (see Table 2). “Becoming ill from the virus” was not only most frequently selected by respondents, but it exceeded other worries by a wide margin. Forty-three percent of respondents selected “Becoming ill from the virus” as one of their top three concerns, while 27% of respondents selected the next most common worry, “Children missing school/child care,” as a top three concern.

In smaller numbers, Georgia adults worry about many other issues, including: decreased value of retirement savings (20%), job loss and resulting loss of health coverage (20%), unavailability of COVID treatment if they or a family member gets sick (14%) and something else (16%).

Though the increased availability of COVID-19 vaccines may have somewhat lessened worries surrounding the virus, it is important to note that over half of respondents remain somewhat or very worried.

Dissatisfaction with the Health System and Support for Change

In light of these healthcare affordability and COVID concerns, it is not surprising that Georgia adults are generally dissatisfied with the health system. Statewide:

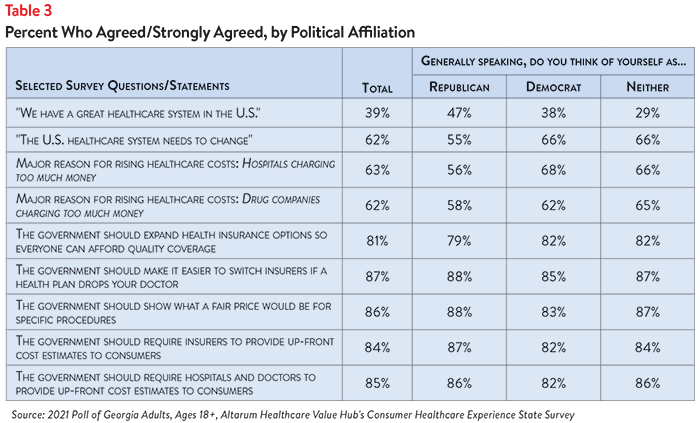

- Just 39% agreed or strongly agreed that “we have a great healthcare system in the U.S.,”

- While 62% agreed or strongly agreed that “the system needs to change."

The survey asked about both personal and governmental actions to address health system problems.

Personal Actions

Georgia adults see a role for themselves in addressing healthcare affordability. Respondents reported specific actions they have already taken, like researching the cost of a drug beforehand (67%), as well as action they should be taking—69% said they would switch from a brand to an equivalent generic drug if given a chance.

When asked to select the top three personal actions that would be most effective in addressing healthcare affordability (out of ten options), the most common responses were:

- 67%—Take better care of my personal health

- 38%—Research treatments myself, before going to the doctor

- 35%—Do more to compare doctors on cost and quality before getting services

Government Actions

But far and away, Georgia residents see government as the key stakeholder that needs to act to address health system problems. Moreover, addressing healthcare problems is a top priority that Georgia residents want their elected representatives to work on.

At the beginning of the survey, respondents were asked what issues the government should address in the upcoming year. The top vote getters were:

- 56%—Healthcare

- 51%—Economy/Joblessness

- 36%—Immigration

When asked about the top three healthcare priorities the government should work on, top vote getters were:

- 41%—Address high healthcare costs, including prescription drugs

- 33%—Improve Medicare, coverage for seniors and those with serious disabilities

- 31%— Preserve consumer protections preventing people from being denied coverage or charged more for having a pre-existing medical condition

- 31%—Get health insurance to those who cannot afford coverage

Of more than 20 options, Georgia adults believe the reason for high healthcare costs is unfair prices charged by powerful industry stakeholders:

- 63%—Hospitals charging too much money

- 62%—Drug companies charging too much money

- 61%—Insurance companies charging too much money

When it comes to tackling costs, respondents endorsed a number of strategies, including:

- 87%—Make it easy to switch insurers if a health plan drops your doctor

- 86%—Show what a fair price would be for specific procedures

- 85%—Require hospitals and doctors to provide up-front cost estimates to consumers

- 84%—Require insurers to provide up-front cost estimates to consumers

Support for Action Across Party Lines

What is remarkable about these findings is high support for change regardless of respondents' political affiliation (see Tables 3 and 4).

Policies to Address COVID Concerns

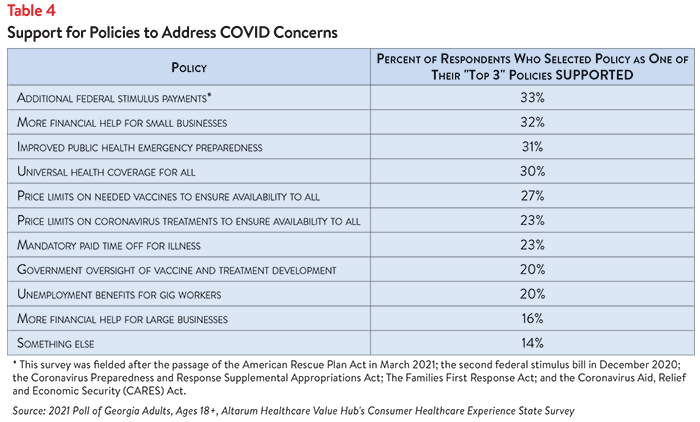

In addition to their views on the policies and approaches above, respondents were asked about support for and against policies related to the COVID crisis. Out of eleven possible responses, respondents were asked to pick the top three policies that would help address COVID-related problems. There was significant diversity in the policies supported, with the highest percentages of respondents selecting “Additional Federal stimulus payments” and “More financial help for small businesses” as a top three priority (see Table 4). The next most supported policies—“Improved public health emergency preparedness” and “Universal health coverage for all”— received nearly equal levels of support. “More financial help for large businesses” received the least support, as it was a priority for only a small percentage of respondents.

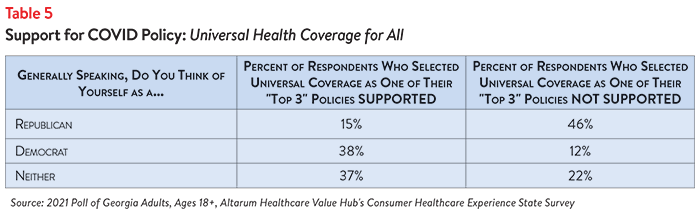

When respondents were asked about which policies they did NOT support, 29% indicated that they did not support “More financial help for large businesses.” Trailing behind that (with 26% of respondents selecting) was “Universal health coverage for all,” although a higher percentage of respondents indicated support. In this area, there was a lack of agreement across party lines, with Republicans far more likely to NOT support “Universal health coverage for all” as a means to address COVID-19 concerns, compared to Democrats and those not affiliated with either party (see Table 5). It is important to note, however, that when asked generically about “Expanding health insurance options so that everyone can afford quality coverage,” 81% of respondents agreed or strongly agreed with this policy as a means of improving affordability, with high levels of support across party lines (see Table 3).

When asked about the policies they did NOT support, respondents were given the option of selecting “I support all of the policies listed.” Twenty-seven percent of respondents selected this option.

The high burden of healthcare affordability, along with high levels of support for change, suggest that elected leaders and other stakeholders need to make addressing this consumer burden a top priority. Moreover, the current COVID crisis is leading state residents to take a hard look at how well health and public health systems are working for them, with strong support for a wide variety of actions. Annual surveys can help assess whether or not progress is being made.

Notes

1. Georgia Department of Public Health, “Georgia Expands COVID Vaccine Eligibility,” Press Release (March 24, 2021).

2. Kaiser Family Foundation, State COVID-19 Data and Policy Actions, San Francisco, C.A. (June 14, 2021).

3. Georgia Department of Public Health, “County Indicator Reports,” Atlanta, G.A. (April 19, 2021).

4. “Gov. Brian Kemp Lifts Most COVID-19 Restrictions for Georgia Businesses with Latest Executive Order,” Gwinnett Daily Post (April 30, 2021).

5. Of the 58% of Georgia adults who encountered one or more cost-related barriers to getting healthcare during the prior 12 months, 28% did not fill a prescription, while 27% cut pills in half or skipped doses of medicine due to cost.

6. Median household income in Georgia was $58,700 (2015-2019). U.S. Census, Quick Facts. Retrieved from: U.S. Census Bureau QuickFacts: Georgia

7. COVID-19 is the disease caused by the coronavirus, which was characterized as a pandemic by the World Health Organization on March 11, 2020. For a comparison of how respondents from Connecticut, Kentucky, Mississippi and New Jersey answered our COVID questions, please see Healthcare Value Hub, How COVID Has Shaped Residents’ Broader Attitudes Towards the Health System, Data Brief No. 86.

Methodolology

Altarum’s Consumer Healthcare Experience State Survey (CHESS) is designed to elicit respondents’ unbiased views on a wide range of health system issues, including confidence using the health system, financial burden and views on fixes that might be needed.

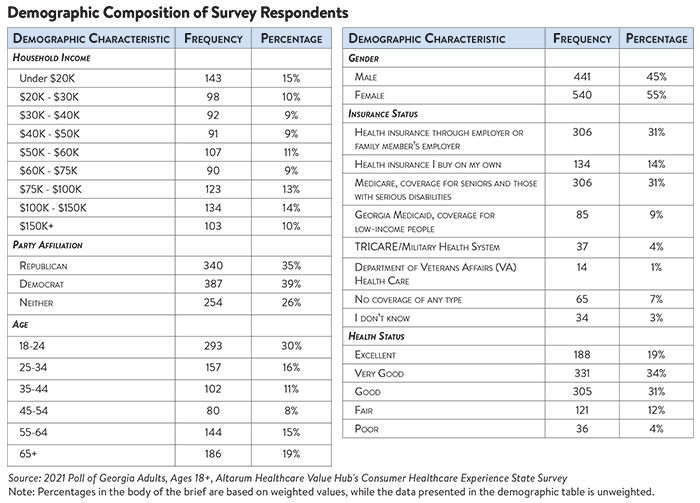

The survey used a web panel from Dynata with a demographically balanced sample of approximately 1,000 respondents who live in Georgia. The survey was conducted in English or Spanish and restricted to adults ages 18 and older. Respondents who finished the survey in less than half the median time were excluded from the final sample, leaving 981 cases for analysis. After those exclusions, the demographic composition of respondents was as follows, although not all demographic information has complete response rates:

Georgia Survey Results

Statewide Reports

Prescription Drug Affordability

Regional Reports

East

Metro Atlanta

North

Southwest

Report Download

|

HEALTHCARE VALUE HUB

The Healthcare Value Hub can help you find free, timely information about policies and practices to achieve health systems that are equitable, affordable, and focused on the goals and needs of the people the system is meant to serve.

Share

![]()

![]()

![]()

Follow

![]()

![]()

![]()